Shepherd Outsourcing opened its doors in 2021, and has been providing great services to the ARM industry ever since.

About

Address

©2024 by Shepherd Outsourcing.

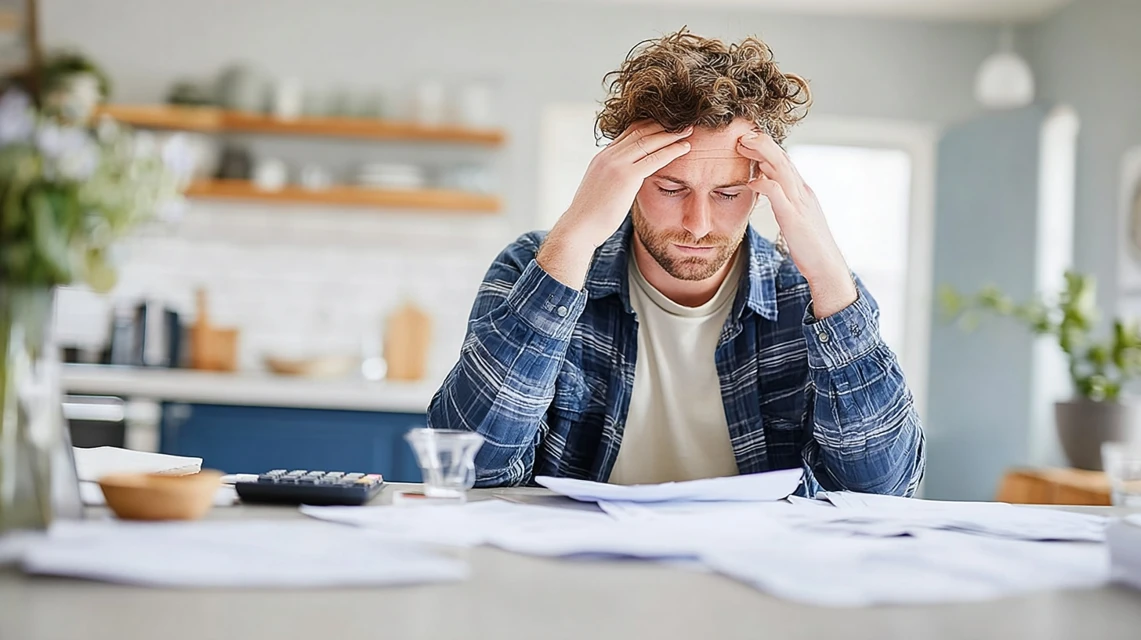

If you’re feeling weighed down by debt and not sure where to turn, credit counseling could be the light at the end of the tunnel. This service, offered by both nonprofit and for-profit organizations, guides consumers through budgeting, managing debts, and planning for a financially stable future. Credit counselors act as trusted advisors, working with creditors to try to reduce interest rates and fees, making it a bit easier for people to pay off their debts without the drastic step of bankruptcy. Curious about how credit counseling works and whether it might be right for you? Let’s dive in to understand what credit counseling involves and how it might help you regain control over your finances.

Credit counseling offers advice on consumer credit, money management, debt management, and budgeting to customers who can feel overburdened by debt. If a person is having trouble repaying their debts, the majority of credit counseling is to help them avoid filing for bankruptcy.

A lot of counseling agencies will attempt to lower interest rates on loans and credit cards and eliminate late fees by negotiating with creditors on the borrower's behalf. Notwithstanding the existence of for-profit credit counselors, the majority of credit counseling organizations are nonprofit, according to the Consumer Financial Protection Bureau (CFPB).

When a consumer's debt becomes too much to handle, credit counseling may be a solution. These borrowers, in contrast to individuals who are about to file for bankruptcy, can typically make at least the minimal payment. The objective is to engage with a credit counselor to create a sustainable financial plan and settle their debts in order to get back on track. Additionally, it assists debtors in developing their budgeting and debt management abilities.

Staff members at reputable credit counseling businesses are certified and trained. These counselors are available to help clients create a customized plan for their credit problems. The average length of an initial therapy session is one hour, and follow-up appointments are offered. A respectable organization ought to provide free information about its offerings without asking prospective customers to divulge specifics about their circumstances.

A debt management plan (DMP), which enables you to make a single monthly payment toward your debt, can be created with the assistance of credit counseling firms. The consumer makes monthly contributions into an account maintained by the credit counseling company under a DMP. The money is used by the group to settle unsecured debt, including credit card, school loan, and medical debts.

The consumer and the counselor work together to create a timetable for these debt payments. In certain situations, creditors may choose to eliminate fees or reduce interest rates, but they usually have to accept the planned repayment schedule. It takes consistent, on-time payments for a DMP to be successful. Completing a DMP could take up to 48 months.

Important: Be cautious of companies that request an upfront fee or service charge if you are thinking about settling your debt. There are conditions outlined by the Federal Trade Commission (FTC) that must be fulfilled before you can be billed for debt settlement services.

Numerous nonprofit organizations that provide credit counseling services in-person, online, and over the phone are available. Nonprofit credit counseling programs are run by numerous U.S. Cooperative Extension Service branches, university campuses, military installations, credit unions, and housing authorities. Information from local consumer protection organizations and banking institutions may also be helpful. However, nonprofit designation does not imply that services are genuine, free, or reasonably priced.

High costs are charged by some credit counseling businesses, which they may conceal. There are others who might encourage customers to donate to their charity.

Understanding any fees you might incur and their purpose is crucial when thinking about using any credit counseling program.

Warning: Prior to filing for bankruptcy, you should consider all of your debt management options because it can seriously harm your credit.

Depending on your needs and circumstances, credit counseling may be able to assist you in paying off your debt. Let's say, for instance, that you are having trouble coming up with a sensible budget. If so, a credit counselor can examine your income and expenses and assist you in finding areas for improvement so that you can generate additional funds for debt repayment.

To assist you in selecting the debt repayment plan that best suits your needs, a credit counselor can also go over several approaches. They might assist you in comparing the advantages of the debt avalanche and snowball approaches, for instance. In order to use either strategy, you must prioritize your debts and make the largest payment on the first one while making the smallest payment on the remaining ones.

How you arrange your debts is where they diverge. You settle debts with the highest interest rates first, then the lowest, using the debt avalanche. Over time, this strategy can help you save money on interest. You pay off your bills using the debt snowball method, starting with the one with the lowest balance. If you can pay off one or two debts quite fast, you may be inspired to continue paying off debt even though you may not save as much on interest.

What you can afford given your income, spending plan, and general financial status will determine whether using a credit counselor is a good strategy to pay off debt. For instance, debt settlement may be an option if you have some savings but are unable to make your monthly debt payments. Additionally, filing for bankruptcy might be the last option in a grave financial position.

Tip: Whether you have concerns about the reputation of a credit counseling firm, you might want to check with your state's consumer protection agency or attorney general's office to see whether there have been any complaints against a specific business.

Consumers and nonprofit credit counselors can be connected through the National Foundation for Credit Counseling. Pre-bankruptcy counseling agencies that have been authorized to offer credit counseling services are listed by the U.S. Trustee Program. Anyone who files for bankruptcy is required by law to first receive credit counseling.

There are some things to look for while looking for a credit counselor that will help you select a trustworthy person to work with. Among the most crucial questions to pose are the following:

You may choose the credit counseling firm you want to work with more intelligently if you ask these kinds of inquiries.

For certain borrowers, credit counseling could be a boon. However, bear in mind that there are some disadvantages to this kind of service. Below, we've highlighted some of the primary benefits and drawbacks of credit counseling.

The fact that you are receiving the assistance you require is the primary advantage of enrolling in a credit counseling program. For many people, budgeting, spending control, and debt management can be intimidating, particularly during difficult times. A financial expert can help you get back on track and create a strategy for a better financial future by guiding you through a repayment plan. You may get back on track and create a plan for a better financial future by asking a financial expert to help you with a repayment plan.

A lump sum payment is made to the credit counselor each month as part of a debt payback plan, as previously mentioned. According to the plan, money is taken out of that account to pay your creditors. This implies that instead of paying several creditors at once, you simply need to make one payment to one location.

Most of the time, creditors want to work with borrowers to pay back their loans. Therefore, in many situations, counselors can help you pay off your debts more quickly by lowering interest rates and possibly getting (late) fees reduced.

Credit counseling has several drawbacks, one of which is that it may have an impact on your credit record. A notation stating that you are enrolled in a credit counseling debt management program may be added to your report by certain agencies. This implies that if you choose to raise any current credit limits or request for new credit, your creditors may view this information. You can be rejected by some lenders if they notice this on your credit record. Before enrolling, make sure to inquire with the credit counselor about the ramifications.

You must close accounts that are considered to be a component of the debt repayment strategy. Even in an emergency, you might not be able to access any more available credit, which is a drawback even though it might prevent you from incurring more debt.

It is crucial to remember that organizations that provide debt settlement or debt consolidation services are not the same as credit counseling firms. Although there may be some similarities between these services, they are not the same.

In debt settlement, a reduction in the total amount of debt owed is negotiated. You have two options for handling this: you either work with a debt settlement company or do it yourself. There is usually a cost associated with the latter choice. Although debt settlement can help you avoid bankruptcy by removing obligations for less than what is owed, it may have a detrimental effect on your credit score.

In order to pay off all of your current debts, you must first take out a consolidation loan. Following that, you would continue to make payments on the new loan in accordance with the conditions and interest rate established by the lender. Although you can't pay less than what is due on your loan using this technique, it can make the process of paying off your debt easier and more convenient. Your credit score will also be far better off with consolidation than with debt settlement.

Credit counseling could be a good option if you are having trouble managing your debt but are not in danger of filing for bankruptcy. This is enlisting the aid of a qualified organization that can intervene. You can erase your debt by creating and following a plan with the assistance of a credit counselor. Remember that the agency may appear on your credit record that you are using their services, even if it might not have an effect on your credit score. Inquiring with the agency about whether it reports to the credit agencies is always a smart idea.

©2024 by Shepherd Outsourcing.